Tokenization and The Future of Money: Improving the old, Enabling the new

And, we should thank cryptocurrency for blazing the way, but the future of finance is likely to be built on tokenization and unified ledgers.

A new paper from BIS (Bank for International Settlements) outlines a “Blueprint for the future monetary system: improving the old, enabling the new”. Within it, the authors outline how the tokenization of money and assets can be scaled out of their existing silos and integrated with a central bank. This approach aims to provide a unified ledger that binds central bank currency, tokenized deposits, and tokenized assets into a programmable infrastructure.

Overall, the paper defines tokenization as “ the process of representing claims digitally on a programmable platform”. These allow intermediaries (such as your bank) to act on behalf of clients, without the traditional separation of messaging, reconciliation, and settlement.

The paper outlines that “crypto” (aka cryptocurrency) can be a flawed model of transacting — as it often does not have any real contact with the real world of banking. At present, most citizens still trust their banks to conduct their monetary transactions, and where cryptocurrency exchanges can still have significant risks. A loss of a private key in a digital wallet can cause someone’s cryptocurrency to be stolen or lost forever, but a loss of your bank details is likely to be resolved through customer support.

Along with this, there is no real link between “crypto” and central banks. The usage of stablecoins provided some advancement, but they cannot truly replace the power of fiat currency — and are typically not private in their usage. But, a method of providing a tokenized settlement asset for a central bank digital currency (CBDC) could provide the answer.

When it comes down to basics, the CBDC model basically allows clients to interact with intermediaries (“their banks”), and then for a tokenized version of a transaction between intermediaries to be recorded on a unified. This could move money into the 21st Century, and get away from our siloed methods of the past.

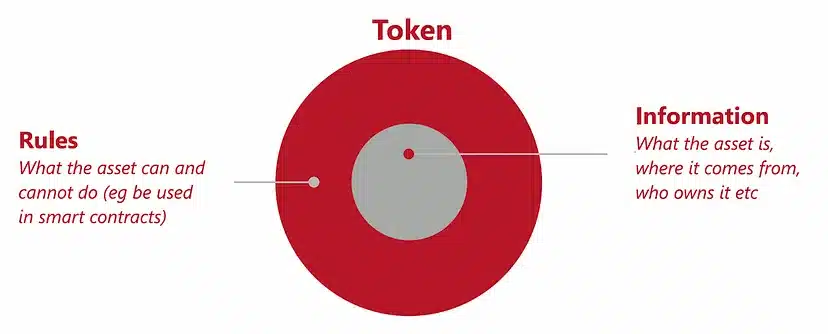

A token is a method of linking an asset to a cryptographically signed entity. Basically, Bob can have a token for the ownership of his car, and then be able to digitally sign the transfer of this car to Alice. Alice will then have proof — on a ledger — that Bob signed the ownership of the car to Alice. When Trent asks Alice about the ownership of the car, Alice can show him the ledger entry of the transfer. The digital signing of the asset transfer will have been conducted with Bob’s private key, and proven with his public key. So, rather than a database of transfers, we can now just have a register that contains all the tokenization transfers.

At any point in time, we can show the ownership of any car. But, now let’s say that we now have a car dealer in-between and who will transact the sale. We do not want the car dealer to have ownership of the car — as they may steal it — so Bob can provide the deal with a claim to the ownership of the car, and that Alice should now be the new owner. A central broker can then agree to the claim, and record it on the central ledger. Each dealer would have their own record for the claims, and these would then be bound in the broker’s ledger.

The overall governance of the infrastructure is provided by the unified ledger, with central banks and regulated private participants. The central bank then has a key role in defining the ultimate settlement asset to a provider. The ownership of assets will thus be recorded on the unified ledger, thus we need to move sure there is privacy built into transactions. The regulated private participants are then responsible for this privacy.

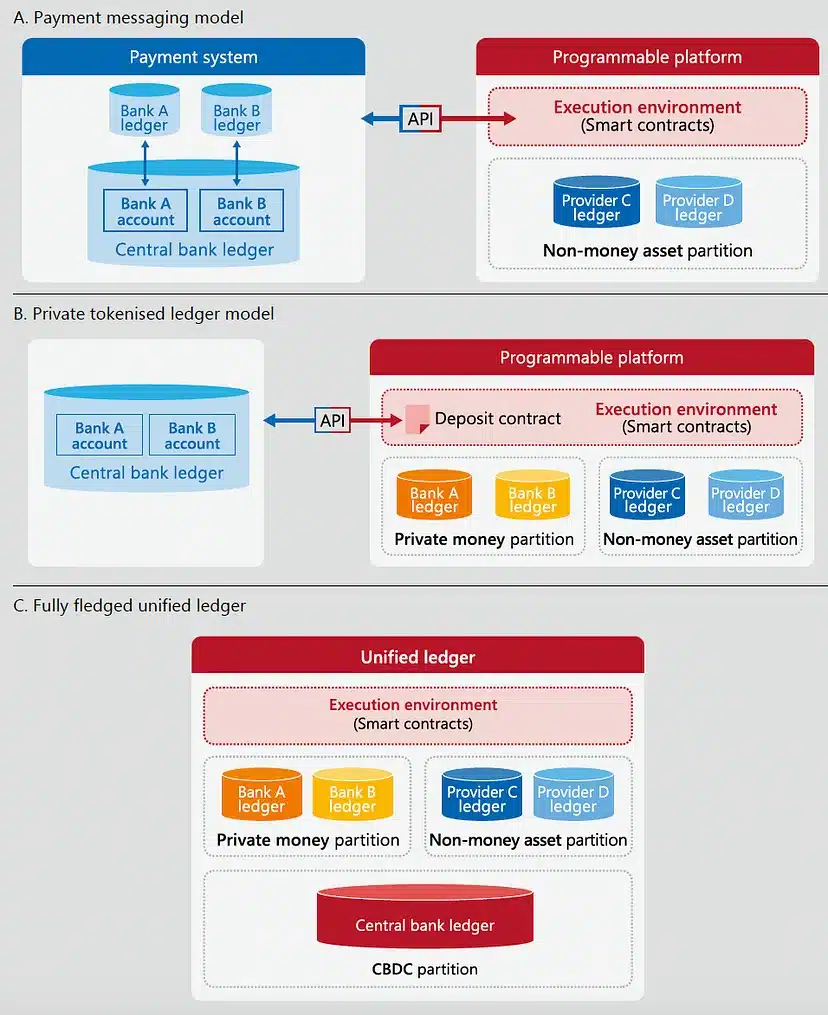

Figure 2 shows three different models that could support the migration toward a unified ledger. In A, we see that each bank has its own ledger, and where we have a partition with provider ledgers. Transfers are conducted through an API interface. In B, we now have tokenized private monies and tokenized assets defined within the programmable platform, whereas in C, we see a unified ledger for all the transactions.

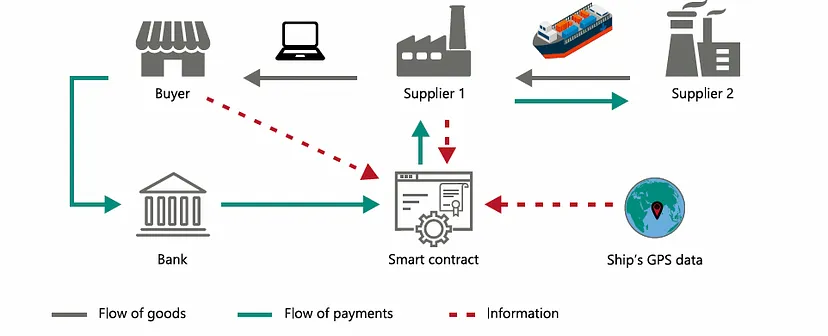

One of the core advantages of using a tokenized version of transfers is in its programmability. In Figure 3, we see a complete transfer for a Buyer purchasing from a Supplier. Overall a smart contract can interact with each of the stages of a contractual payment so that the bank could commit funds to a purchaser from a Buyer, but not release it until the goods have been delivered.

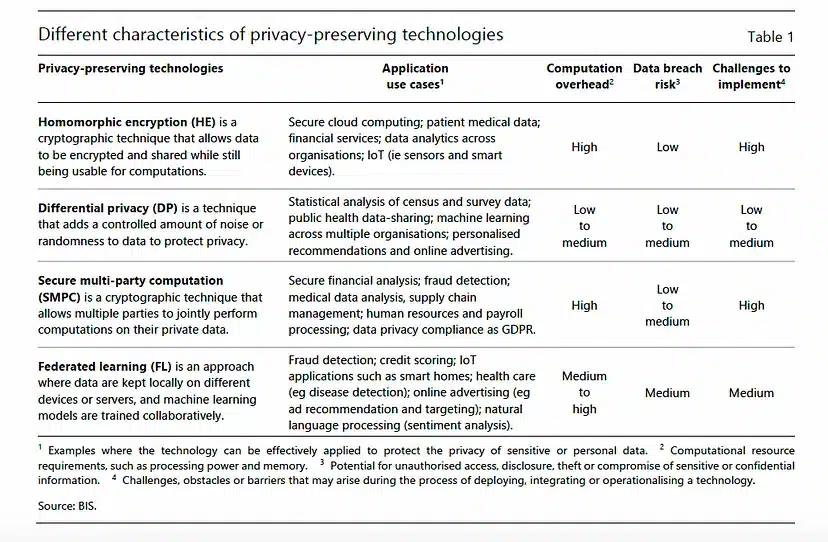

The paper poses some methods that can be used to ensure privacy, including with homomorphic encryption and differential privacy (Figure 4). We can see that homomorphic encryption has the lowest data breach risk, but has a high computation overhead, while differential privacy has a low computational overhead, but a low to medium risk for data breaches.

And here are the outline plans in the UK for a digital pound

Conclusions

The whole blockchain debate is over. Public key encryption will build a more robust world of transactions and is now being used at scale to build new economic models. “Crypto” has blazed the way, but it is tokenization that will see us build a more trusted world of finance.

Welcome to the future! Improving the old, Enabling the new.

Photo by Tomasz Frankowski on Unsplash

Read other stories: 1ST blockchain hackathon set to take place during European Blockchain Convention 9

Tokeny and Klaytn Foundation Unite for Massive RWA Tokenization Adoption in Asia

You Might also Like

Sponsors

Related Stories