The FATF (Financial Action Task Force) has recently issued a new set of guidelines which are applicable to the crypto sector, mainly with regard to Virtual Assets (VA) and Virtual Assets Service Providers (VASPs). But let´s bring some order into something that might otherwise be slightly confusing and which implications have generated some degree of alarm in the crypto community.

Guest post by Andrea Bianconi

What is FATF

This financial task force was created back in 1989 by the then G7 ministries to set standards and promote the implementation of legal, regulatory and operational measures for combating money laundering, terrorist financing and other related threats to the integrity of the international financial system. The FATF is not a legislative body, it does not have binding regulatory power, it is therefore merely a“policy-making body” which works to generate the necessary political will to bring about national legislative and regulatory reforms in these areas. Its guidelines are just that, guidelines, which means they are neither laws nor regulations and are not binding for anyone until they are adopted and implemented within national jurisdictions by member states. However, FATF power shall not be underestimated. In fact, member states who do not comply with its guidelines could be blacklisted and therefore subjected to stricter controls in their interactions with other countries within the legacy financial system. At present only two countries, Iran and North Korea, are blacklisted while a number of other countries are being closely monitored, among them Panama, Syria, Bahamas, Pakistan and Tunisia. Since 1989 FATF has grown into a network of 38 member countries covering over 200 jurisdictions worldwide thanks to a number of affiliate organizations. Its reach is undoubtedly global.

Recommendations and Guidelines

FATF has operated by releasing a set of Recommendations and subsequent interpretative guidelines. The latest set of Recommendations was released in 2012. Periodically then — whenever new developments arise — it is necessary to re-interpret the Recommendations based on the new developments. Therefore new interpretative guidelines are regularly released. In February 2019 an Interpretative Note was issued, which then became final in June 2019 when this new set of guidelines — dealing with VA and VASPs — has been released.

Background — Virtual Assets and Virtual Asset Service Providers

This new set of guidelines is applicable to VAs and VASPs as they were defined in the previous October 2018 guidelines.

Just to recap, a Virtual Asset is a digital representation of value that can be digitally traded or transferred and can be used for payment or investment purposes. The guidelines exclude digital representations of fiat currencies such as e-money or stablecoins, as well as security tokens or other financial instruments already covered elsewhere by the recommendations. Cryptocurrencies — such as BTC, ETH or XMR — and various types of non-security tokens are falling under the guidelines. As far as utility-tokens are concerned, it seems that the deciding factor which makes the guidelines applicable or not — according to para § 47 — it is whether a token is transferable, exchangeable, fungible or not. Indeed FATF clarifies that it does not seek to capture the types of closed-loop items that arenon-transferable, non-exchangeable, and non-fungible…such as airline miles, credit card awards, or similar loyalty program rewards or points, which cannot be sold in a secondary market.

Virtual Asset Service Providers are defined as natural or legal persons who carry out one or more of the following business activities:

i) exchange between VAs and fiat currencies;

ii) exchange between different VAs;

iii) transfer of VAs

iv) safekeeping and/or administration of VAs or instruments enabling control over VAs

v) participation in and provision of financial services related to an issuer’s offer and/or sale of VAs.

The above definition is wide enough to include exchanges and transfer services, wallet providers, custodial services such as those that host wallets or maintain custody or control over another person’s VAs, wallets, and/or private keys, as well as providers of financial services to an ICO.

But that´s not all. Included might be escrow services, like those involving smart contract technology, when the entity providing the service has custody over the funds; brokerage services that facilitate the issuance and trading of VAs; order-book exchange services, which bring together orders for buyers and sellers, typically by enabling users to find counterparties, discover prices, and trade, potentially through the use of a matching engine for buy and sell orders; and advanced trading services such as trading on margin or algorithm-based trading.

How VASPs will be impacted by the Guidelines

The guidelines update and impact in particular the existing Recommendations nr. 10 and 16.

Under Nr 10 the threshold above which VASPs should carry out a customer due-diligence for the purpose of AML/TF (Anti Money Laundering/Terrorist Financing) is lowered to a transfer of merely €ur/US$ 1.000, instead of the normal €ur/US$ 15.000 applicable to fiat transfers.

Under Nr. 16 the VASP of the transferor must identify and collect all personal information about the transferor and share it with the VASP of the transferee. The same should do the VASP of the transferee. Basically both parties to a transfer must be identified (just like it happens with bank wire transfers).

Comments and practicalities

Frankly, I miss the rationale behind the above provisions which are mostly unenforceable and of little practical use and which will not adversely impact ML/TF activities but will rather increase compliance costs, needless paper-work and maybe slow down the growth of the crypto sector in those countries which will implement them.

How lowering 15x the threshold for occasional VA transactions can be effective against ML when — facts based — crypto laundering represents only 0,081% of the annual US$ 2 to 4 trillion global fiat money laundering problem?

It is like reducing global CO2 emissions by prohibiting farts.

Moreover, how do you practically identify the beneficiary of a non-custodial BTC address? (i.e a new address of which someone privately holds the keys and not an address at an exchange or broker or custodian). No way.

In addition, this provision will encourage peer-to-peer transfers via non-custodial wallets, which makes it much harder — if not impossible — to track and control for the authorities. For example, I could send funds from an exchange to a non-custodial wallet (where I control the private keys). From that wallet I could then send the coins to a different exchange, and neither platform would see both sides of the transaction.

Conclusions

Unless you believe that the FATF is staffed by grossly incompetent people on crypto related matters, then the only conclusion to be drawn is that the real reasons for implementing both impractical and unenforceable guidelines lie somewhere else.

Is this a try to damage the sector? Is this maybe a clumsy attempt to strengthen the grip of the legacy financial industry on the crypto sector, like they did with the infamous Bit-Licence in New York?

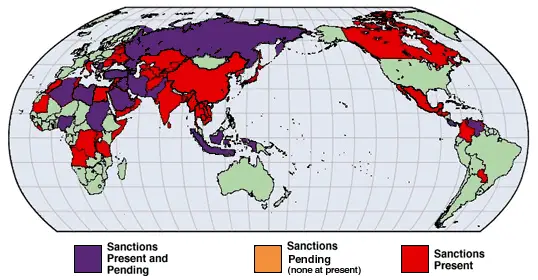

Or maybe is this a US led move to make it more cumbersome for sanctioned countries — such as China, Russia, most of the Middle East, half of Central and South America, half of the African continent and maybe soon also the EU — to circumvent the sanctions by using crypto instead of the greenback?

I ask: Cui prodest?

Time will tell.

Luckily, truly decentralized blockchains (like BTC) were born for that very same reason: to be censorship resistant, resilient and without central points of failure.

Now, the FATF can blacklist financial institutions in non-complying countries. But what the blacklisting of a VASP will practically achieve? Let´s assume X country does not implement the guidelines. Assume also that FATF blacklists a crypto exchange in X country. The blacklisting can only apply to fiat transactions between financial institutions within the legacy financial system which will be subject to more scrutiny. It will affect investors wanting to transfer fiat funds to that exchange.

But as shown in the above examples it cannot affect peer-to-peer crypto transfers and it will not prevent you and any other individual and business from transferring — from any non-custodial address — cryptos to such blacklisted exchange regardless of the sanctions/blacklisting. And vice-versa.

As always, draw your own conclusions.

WRITTEN BY

Andrea Bianconi, a lawyer, consultant, writer and speaker – www.bianconiandrea.com

www.thinkblocktank.org

More Article:

You Might also Like

Related Stories