The future of goods and NFTs

In this interview, Vinay Gupta, CEO and founder of Mattereum, explains how Mattereum helps bring real-world objects to the blockchain via NFTs. Gupta also elaborates on what such NFTs can be used for and gives insights into the machinery of registering objects through Mattereum.

Jonas Kasper Jensen (JKJ): What is Mattereum, and what problem is Mattereum solving?

Vinay Gupta (VG): I developed the idea for Mattereum during the period when I was still at the Ethereum foundation in 2016. The idea was to provide a legal enforceability layer for smart contracts. Suppose you have two parties who make a smart contract together, exchange value on this smart contract, and something goes wrong. In that case, you need a litigation framework around the smart contract that enables people to go to court and recover the value. That layer lets you get out to the real world and tokenise real objects. It allows you to tokenise physical assets and do transactions for things like houses, cars, gold, fine art, clothing and all the kinds of real-world things that people need. At Mattereum, we make all that stuff transferable.

JKJ: Is all information about objects stored through smart contracts?

VG: The smart contract is only one part of the contract. Let me give an example: Think of the sale of a gold bar. The smart contract can indicate who currently owns the bar, but the smart contract cannot describe what the bar is, where the bar is costodied and where the bar was mined. All that information is textual content, it’s just paper. You have to put that paper somewhere where it can be retained and is visible for the duration of the contract. So you typically put it someplace like IPFS, and you have to pin it in the smart contract, which is to say you have to create links from the NFT smart contract to the papers. The transactability is what happens on the chain. The definition of the goods being transacted is in the paper contract. And so you have a hybrid system where you have paper contracts that describe the goods, and then you have smart contracts to tell you who currently owns the goods.

JKJ: When you issue an NFT, for example, for gold, how would that work?

VG: The way it works is that when you transfer the NFT, the buyer pays a fee to a seller. They also pay a fee to Opensea, that is the platform fee, they pay a third fee, which is a small residual payment, which is made to the people that provide information about what they’re buying. And that transaction is a set of warranties. So that’s how, when you buy the object, you know you buy, for example, Timmy Trumpet’s trumpet. The trumpet cost hundred thousand dollars. You buy the trumpet, Timmy and Mattereum, and a few other people all take small transactional fees. And what happens is those create a legal contract because a payment has been made and a contract has been given between the new holder of the NFT and all of the people providing information about what the NFT represents in the physical world. So that gives the person buying the NFT legal rights in the real world because they bought a warrant that gives them real-world protections.

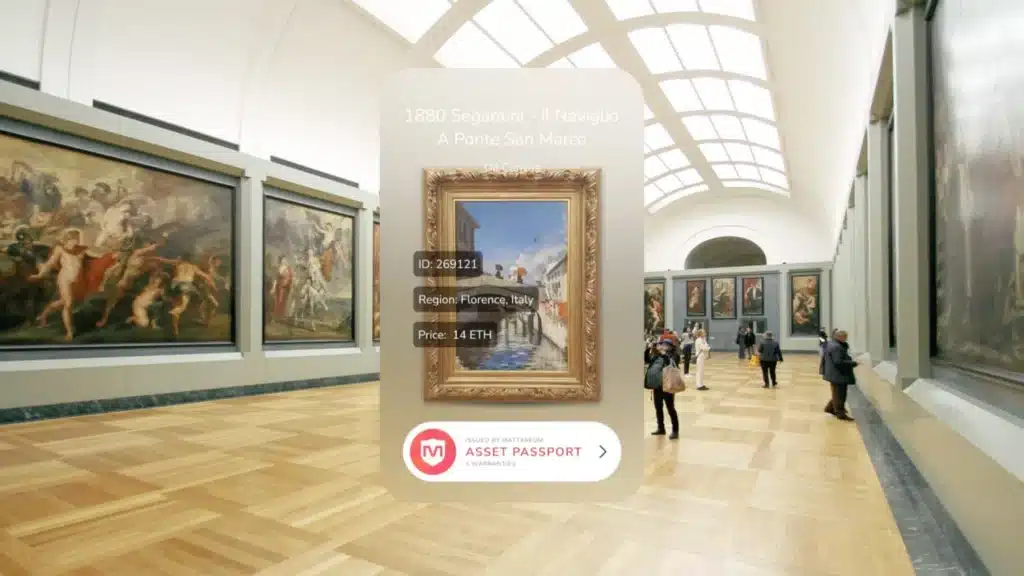

JKJ: Mattereum sometimes uses the term Asset Passport in connection to this process. But what is an asset passport, and how does it prove that the objects recorded through the NFT exist?

VG: On the asset passport for Timmy Trumpet´s trumpet, you can see a set of different warranties. Each one of those warranties is a legal document. These warranties tell you what you’re buying and all its unique features. The asset passport includes the signature logo of Timmy Trumpet, a description of who produced it, when was it made, where was it produced and lots of pictures of Timmy playing the trumpet. Hence, the buyer understands exactly what this thing is. Timmy Trumpet is making a promise that the Trumpet is what you get. All of this information is then bundled up in a legal contract. When you buy the NFT, you pay one-third of a percent of the NFTs price to Timmy Trumpet blockchain enterprises limited. That company is taking this fee, and in return, they will give you up to the total purchase price of the NFT equivalent to the price at the time of purchase. And at that point, you can now legally rely on all of the information when you buy the NFT. That’s what tells you that it’s legit.

JKJ: Typically, NFTs are supposed to be unalterable when minted on a blockchain. Can the asset passport be changed over time, and why would one want to change it?

VG: Say that the object has to be moved to a different vault because that vault is going out of operations, or it has been merged with a different company, or something like that happens. Then the information is now no longer accurate. You haven’t lost any value as a result. It’s not a breach of contract, but the next buyer needs new information to put into the passport. So in that instance, what happens is that one claim is removed. Another claim is that you are a party to the first version of the claim, but when you sell the asset to somebody else, they’re a party to the second version of the claim.

JKJ: Why is the combination of NFTs and digital paperwork superior to the paperwork that has traditionally been used?

VG: It comes down to the execution of the contract. When the NFT changes hands, five of these contracts get executed simultaneously in a single atomic transaction. Everything just switches at the same time, quick payment and all the contracts simultaneously execute, and because of this, the object changes hands in a single atomic swap.

KJ: Would you be able to go in front of a court if there are any disputes over the object sold through the NFT?

VG: In the UK, the court system has gotten very interested in blockchain technology. They published a set of rules called the UK digital dispute resolution rules. All disputes involved in these contracts are heard under the UK digital dispute resolution rules. Have you heard of a thing called commercial arbitration or international arbitration? Under international law, they have special provisions for handling disputes between parties in different countries. If you, for example, are in Australia and you buy a thing from somebody in Hong Kong, if there’s a dispute, the question is, do you use Australian or Hong Kong law to handle the dispute? In the international system, you can specify that the law for this dispute will be Hong Kong or Australian law, but you can also specify English law. And this is called the choice of law. The contract between us specifies what law we will use in a dispute. This is step one.

The second thing is we can also specify which court so we could say it’s held at, if it is held in Australian law, in an Australian court, Hong Kong law, in a Hong Kong court or English law, we could specify in an English court. But if neither you nor I are in England, it’s unclear if an English court would take the case.

So you can then appoint a private judge to hear the case under English law. And that judge is called a commercial arbitrator. This is how very complex issues of commercial property law are typically handled. It’s how maritime disputes are handled. Everything has to do with shipbuilding and oil rigs. You don’t take all these hardcore engineering cases to court with a jury. The jury doesn’t understand what’s happening. They have no expertise. You take them to specialised commercial arbitrators. So we take arbitrators from the pool of arbitrators that are very experienced and nuanced in handling the issues in the law that specifically relate to computers, and the contract between you and I specifies English law under the UK digital district resolution rules with a privately selected judge that will be from this pool of technically sophisticated arbitrators. And those systems together give us access to legal rulings, which are enforceable in all the countries that are handled under the 1958 New York convention on foreign arbitration. So, that structure is comprised of 160 countries and an international treaty signed in 1958, and all of the Mattereum machinery bedrocks down directly onto that treaty.

JKJ: Can you tell more about trustable NFTs in relation to the UK digital dispute resolution?

VG: A trustable NFT is an NFT that is tied to all of this machinery and has a backdoor key for the arbitrator. Under this UK digital dispute resolution framework, a judge can generate a court order to move the ownership of a digital asset if anybody has a key that allows them to do this.

Let’s use Bitcoin as an example. The judge makes an order for Bob to give Harry five Bitcoin. Bob doesn’t have to do a god damn thing, and nobody could force him to. They could sell his house instead of the Bitcoin, but they can’t make him hand over the Bitcoin. Because there’s no technical affordance in the Bitcoin system to allow somebody to move the money. But if I have an ERC-721 contract with a special key to be used for arbitration disputes, then I go to the judge and say, this guy over here hacked my computer and stole my NFT.

Special provisions in the UK digital dispute resolution rules enable a privately appointed judge and arbitrator to move crypto assets if the crypto asset has a key.

So the way that it works is you have code in the smart contract that allows for the transfer of ownership, but that transfer capability isn’t activated until somebody that has owned one of the NFTs puts the NFT contract in a technical state that turns on the arbitrator key. The arbitrator key doesn’t work unless one of the parties raises a dispute and flips the contract into a state where the arbitrator key becomes activated. This is the disputed state. When the NFT enters the disputed state, it can’t be transferred anymore, and it’s locked until the arbitrator unlocks it. When the arbitrator unlocks it, they can transfer it to a new owner. It’s a very powerful system.

JKJ: That is different from what I normally would think of NFTs. Normally you can buy, sell and own NFTs, and you can send NFTs to other people’s wallets, but they are meant not to be altered, and no other person than the owner of the private keys has access to the assets…

VG: Exactly. If you want to be able to use NFTs for real estate, you can’t be in a situation where somebody hacks the contract and steals a five-story apartment building in New York. We’ll never be able to tokenise real estate on that basis.

JKJ: Is it possible to use this method for tokenising real estate through NFTs?

VG: Here we’re dealing with stuff that sits in a weird hybrid state. To the blockchain, it looks like an NFT. For a lawyer, it looks like a contractual obligation managed with digital signatures. Digital signature legislation has been valid in all commercially active states for about 25 years. We’ve had digital signatures for a long time. The law is fully caught up in digital signatures. So if you think of the NFT transfer as being a digital signature of a contract, and then you get something like breach of contract, the whole thing fits inside of a legal framework that lawyers can understand and work with. No ambiguity there. No problem there.

That gets you contractual obligations. You can’t just have a smart contract update a national property rights register. You can’t just say that the government of Finland will change a house’s ownership because a smart contract update doesn’t work. But it does work if you consider it a commercial obligation on a third party. So if you have a corporation that owns a house in Finland and the corporation has a legal responsibility to give the house to whoever owns the NFT. When the NFT owner comes back in and says I would like my house, please, the next thing that happens is that the corporation then updates the national property rights register on behalf of the person that brought the NFT in. The corporation has a contractual obligation to move the NFT and to move the property to match the ownership of the NFT. As long as you have an intermediate corporation with legal ability to the NFT holder, they update the national register.

JKJ: So you need an intermediary. Can’t you just make an NFT and let that be the deed for a house?

VG: You must put the house’s ownership into a corporation. The corporation then handles the transfer of the property, or it simply holds it in trust for the person that is the current owner of the NFT. So this is the other model where the corporation says, if you have the NFT, you can live in the house, but also if you want us to transfer the property ownership, we will give it to you. In that model, you get a simple, straightforward deal where I own the NFT. I bring the NFT to the corporation. The corporation says, here are the keys. If you want us to update the property register and transfer the ownership from us as a corporation to you, we can do that, but then the NFT will be useless. So why don’t you just live in the house and keep the NFT? And then, if you want to sell the house, you just sell the NFT.

JKJ: I see some projects fractionalising NFTs, and you can buy into maybe getting some rent from a house or owning part of the shares of a house. What do you think of this approach to NFTs and real estate?

VG: In general fractionalising things is really difficult. It’s legally difficult because it’s legally dangerous because the minority tends to get screwed by the majority. Think of something like a Stradivarius violin. We work with violins. We’re very close to the violin world. If somebody has a Stradivarius violin and buys 51% of it, you don’t want that violin to be played in the middle of the day in the hottest desert on earth where the wood will crack. We’re never going to let that happen. In that situation, you have to have the minority shareholders control what happens to the asset to protect their investment and the asset.

When we start dealing with things like real estate, if I’m the real estate owner, and there’s a problem with the roof, I will take care of it. It’s my property. If the real estate is owned by 250 people and the roof has a problem, who the hell is responsible? And for that reason, we think that commercially, the fractionalisation of this kind of stuff it’s possible, but it has to happen inside of a disciplined legal environment because otherwise, what you wind up with is the minority getting screwed by the majority or the thing falls into disrepair because nobody pays the maintenance fees.

It’s not that we don’t think this could be done, but we won’t handle it. We will handle the locking of the asset for a single party. If that single party then figures out how they’re going to fractionalise it, they can do that, and we will then support them doing it. But it’s two different functions. The custody function is a separate thing from the fractionalisation.

Learn more about NFTs on NFT by The Tokenizer.

Read other stories: Chintai is granted licence by the Monetary Authority of Singapore to conduct the regulated activity of dealing in capital markets products

SubQuery Powers the Data Behind Polymesh’s Bespoke Security Token Blockchain

You Might also Like

Related Stories